Investment Idea: Estapar is Undervalued

Sem Parar’s Acquisition of Gringo Highlights an Investment Opportunity in Estapar

Disclaimer: I am not an investment advisor. This article is simply an investment idea.

I recently invested in Estapar (ALPK3) after analyzing the deal between Sem Parar and the Brazilian driver app, Gringo. Here’s why I believe this presents an investment opportunity worth sharing with my subscribers.

Sem Parar, a major fintech owned by Fleetcor, recently acquired Gringo for an estimated BRL 1 billion. This is a significant deal, considering Gringo was only founded in São Paulo in 2019. The app provides financial services and digital solutions for thousands of Brazilian drivers. Just six months ago, Gringo raised BRL 70 million in funding.

Key Details of the Sem Parar-Gringo Deal

According to VEF, one of Gringo’s investors, the sale of its stake in Gringo will add US$15.2 million to its balance sheet—the exact amount the fund had invested in the company over the last two years. What????? The same amount as two years ago?

This raises an important question: Was the valuation justified?

VEF held a 9.3% stake in Gringo. Using this percentage, we can estimate that the total valuation of Gringo was around US$163 million (approximately BRL 1 billion). However, without further details on the agreement, it's difficult to determine the precise valuation.

If Gringo, a relatively new app, was valued at BRL 1 billion, what does that mean for Estapar, the leading parking company in Brazil?

To me, the bigger story here isn’t the Sem Parar-Gringo deal—it’s Estapar’s market cap. Something doesn’t add up.

Estapar (B3: ALPK3)

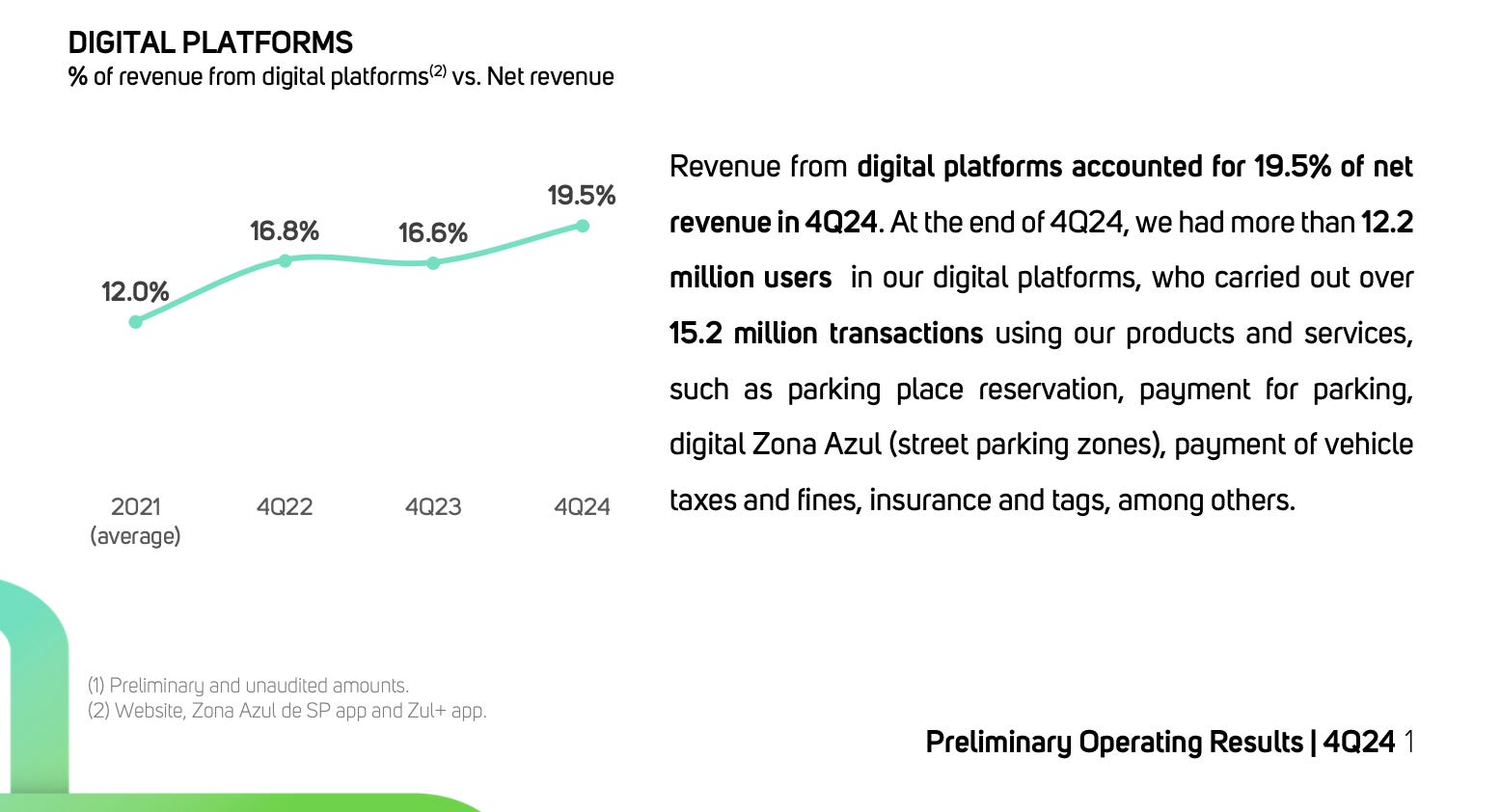

Estapar owns the super app Zul+ (Zona Azul Digital), the leading digital parking platform in Brazil. The company operates in 19 states and more than 97 cities, managing over 700,000 parking spaces and serving millions of customers each month.

Currently, Estapar’s market cap is approximately BRL 600 million, despite having 1.7 million users on its app. According to Estapar’s latest earnings report, Zul+ contributes 19% of the company’s total revenue—around BRL 250 million.

Key Financials

Estimated 2024 Revenue: BRL 1.5 billion

Estimated Zul+ Revenue (2024): BRL 400 million

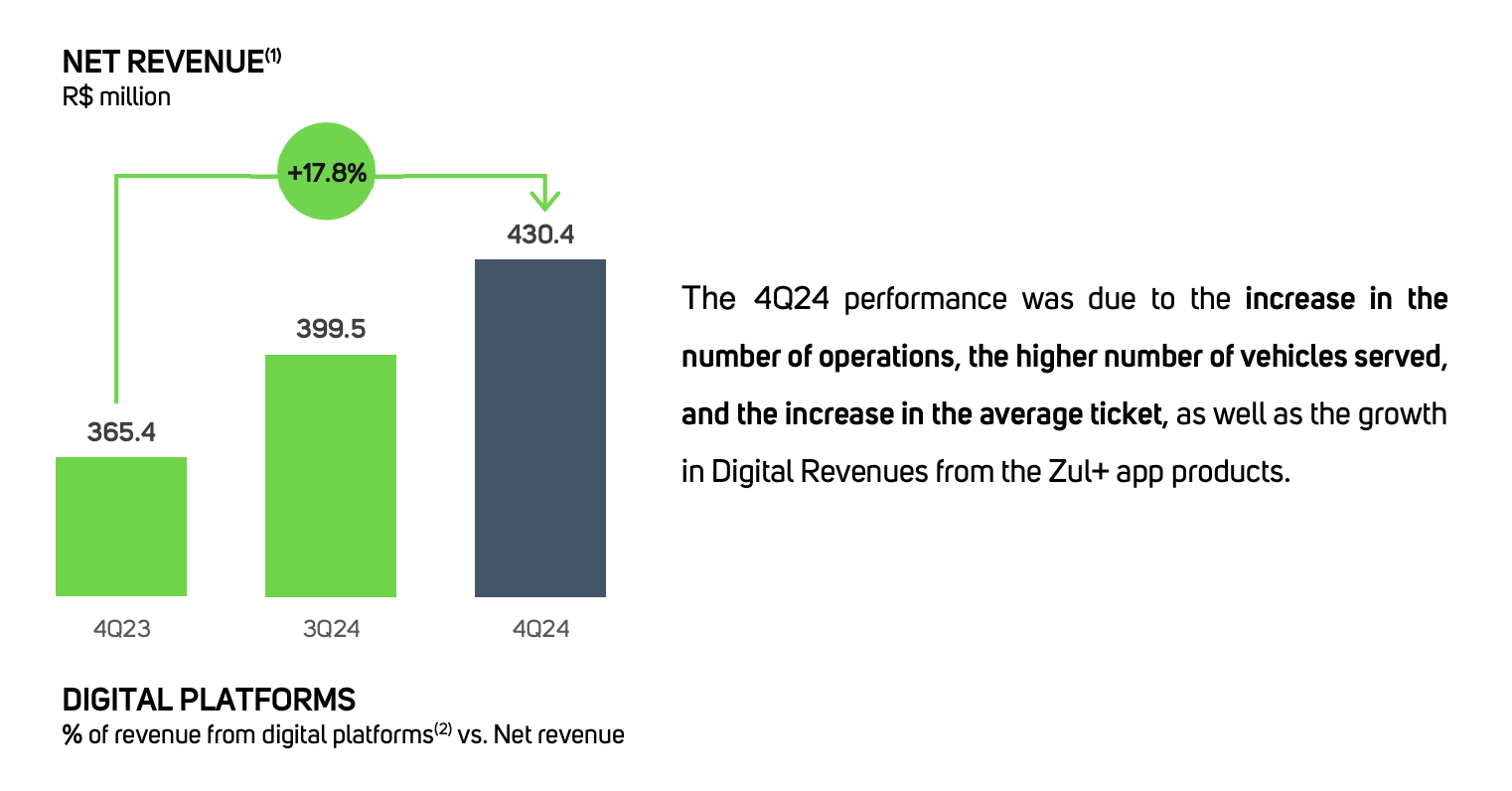

Estapar recently published its preliminary operational results, further reinforcing its strong financial position.

Estapar is Undervalued

This investment idea stems from the apparent valuation discrepancy between Gringo and Estapar. Either Sem Parar overpaid for Gringo, or Estapar’s market cap is significantly undervalued.

Even with the low liquidity of Estapar’s stock, I see a compelling opportunity. The numbers suggest that Estapar’s valuation should be much higher, making it a potential hidden gem in the market.